The Value of Political Markets The betting odds are useful, but they could be better Charles Lipson

https://www.mercatus.org/bridge/commentary/value-political-markets

As the election draws nearer, political junkies pay closer attention to poll numbers. But they are well aware of the difficulties and gaps in those numbers. It’s gotten harder to reach truly random samples of voters and harder to be sure they are giving their true opinions since some opinions risk a torrent of graffiti and social ostracism.

Even if a survey generates a valid random sample and gets voters’ honest opinions, a national poll won’t predict results in the Electoral College, which is expected to hinge on six to eight swing states. Those states need to be polled intensively and the results presented for each individually. Finally, once the raw data is collected, pollsters must make educated guesses about which subgroups will actually show up and vote. These assorted guesses and varied polling methods are why so many observers rely on Real Clear Politics polling averages, compiled from several highly regarded sources.

Besides these averages, political analysts now pay close attention to “political betting markets.” The odds in early September show a tight race—making Democrat Joe Biden a favorite to win the presidential race, but only by a few points.

How Do Betting Markets Supplement the Polls? Are the Markets Better?

Betting odds are generally more accurate forecasts than polls because the odds incorporate all polling data plus any other relevant information. Bettors might notice that President Trump is suddenly drawing larger crowds than before or that Biden raised far more in donations than expected. That information won’t necessarily be reflected in poll numbers, and it certainly won’t show up right away. But it figures immediately in the odds since it matters for the candidates’ chances in November.

The scholarly literature reaches the same conclusion. “Prediction markets are an effective means to forecast elections,” as one review puts it. “Evidence to date shows that markets often provide more accurate forecasts than established benchmark methods such as polls, quantitative models, and expert judgment.” The more extensive the markets, the more efficiently they incorporate all relevant information.

Political markets, like those for stocks, next week’s interest rates, or next month’s delivery of West Texas Crude Oil, involve people making bets about which direction prices will move. When they make those wagers, they use all the information at their disposal. That information changes minute by minute, hour by hour, as events unfold. In political markets, the odds would change immediately if Biden appeared confused at a press conference—or, rather, if he appeared more confused than usual. “The usual” is already built into the odds.

What changes the odds is any new information that is expected to drive voter behavior. When The Atlantic ran a particularly damaging article about Trump disparaging soldiers, what mattered was not the magazine’s small readership or rebuttals by conservative websites. What mattered for political markets was that mainstream media began running it as their lead story. Their heavy promotion hurt Trump in two ways. First, it undermined one of his strongest claims: that he is the military’s strongest supporter. Second, it signaled that the mainstream media might launch a nonstop series of high-profile pieces heavily critical of Trump between Labor Day and the election.

It’s possible the markets simultaneously picked up other information weakening Trump’s position or improving Biden’s. It’s always hard to know exactly what moves markets—or odds. In any case, the effect was swift. The odds against Trump shifted immediately, just as they would if Microsoft announced higher-than-expected profits or if a top quarterback were injured in practice. The odds (or prices) already reflect known information, such as the quarterback’s health and expected performance. What shifts the odds is new information that could affect the outcome in question, such as a football score, a stock price, interest rates, or a candidate’s chance of being elected.

Political markets will also parse breaking news, such as newly reported numbers on coronavirus deaths or weekly unemployment claims. The odds will shift depending on whether bettors think the numbers benefit the incumbent or the challenger. For some events, it’s hard to know who benefits most. Do urban riots favor Trump (who promotes law and order) or Biden (who emphasizes inequality and racial justice)? Do the protests distract from Trump’s economic message or harm him because the incumbent is ultimately held responsible for the country’s condition?

Will the riots change voter behavior? Does it matter if they happen in places like Kenosha and Rochester, rather than Portland and Seattle? The answers are far from obvious, and they won’t show up in polls for several weeks. Before then, bettors will make their own guesses, tweaking the odds. When they see the latest poll numbers, they will update those guesses, tweaking the odds once again.

One value of betting markets is that the odds change immediately, just as they do for stock prices and futures markets. The next poll might not come out for several days. It might take a week or more for the new information to be fully reflected in polling averages. The betting odds, by contrast, are instantaneous.

How does important nonpublic information figure in the polls and odds? It is completely missing from the polls, by definition. If voters know something, then it’s public information. Whether any hidden information appears in betting markets depends on whether those who possess secrets can make significant wagers based on their covert knowledge. If they can, then the secrets affect the odds, even if the public doesn’t know their content. If the secrets don’t affect the odds, then either they are irrelevant or the bettors can’t make use of them.

Put differently, do the secrets really matter for the outcomes in question, and can those who possess secrets take advantage of them? It’s illegal to use nonpublic information in financial markets, though some insiders still chance it. In political markets, however, the limitation is different; it’s that people who possess inside knowledge cannot make large bets on it. That means the odds do not fully reflect that private information.

Some private information might creep in, even though the bets are small, because the political markets are so much smaller than those for stocks, commodities, and sporting events. In small markets, even small bets can have some impact on the odds. Not so for championship fights or the Super Bowl, where billions are wagered.

The Limitations on Betting Markets

The political markets are small because federal laws severely restrict them within the United States and prevent Americans from betting on our politics in foreign venues, such as English bookmakers (which accept bets on US elections but not from Americans). Those are consequential limitations. After all, it is Americans, not some punters in a Leeds pub, who are most likely to uncover new information about Trump or Biden, or whether incumbent senators from Maine or Colorado are likely to retain their seats. But the laws currently prohibit Americans from making large wagers based on that inside knowledge. That also means bettors have no incentive to acquire such knowledge.

To understand why these restrictions matter, imagine that there are ultimately two classes of bettors. Some are small fry who enjoy making minor bets. Actually, they don’t have better information than the guy on the next barstool. They can be called “noise” bettors because they add noise, not real information, to the betting market. The second class of bettors is far better informed. They read polls carefully, talk to campaign managers, volunteers, and reporters, and perhaps speak with the candidate himself. Armed with that knowledge, they make more accurate assessments, on average, than noise voters and make a living by winning bets. Let’s call them “signal bettors.”

If these shrewd “signal bettors” could wager millions, their information would drown out the noise, as it does in markets for interest rates and oil futures. In political markets, however, well-informed players cannot make large wagers so there is less signal and more noise reflected in the odds. It’s unclear how large this effect is and whether it imparts any bias. (It wouldn’t matter, for instance, if small, “noise bettors” were on opposite sides and canceled each other out.)

Why does the depth of these markets matter? Why does it make odds for political events less informative than those for, say, crude oil futures or pro football games?

Consider an upcoming game between the Green Bay Packers and the New York Giants. Let’s assume, accurately, that small bettors like to bet on their hometown team. Given New York’s much larger population, that means there will be lots more $100 and $500 “hometown” bets on the Giants than on the Packers. That would skew the odds unduly toward the big-town team unless a lot of smart bets for the Packers came in from Atlanta, Phoenix, and Seattle. Without those outside bets, you could consistently make money by betting on teams from smaller markets like Green Bay, Pittsburgh, Cleveland, and Cincinnati and betting against New York and Philadelphia. It’s not that the small-market teams are better; it’s that the betting line doesn’t accurately reflect their chances.

Does betting on the small-town team actually work? No. The markets are too deep and efficient. If, for some reason, the odds don’t reflect all information available to well-informed (“signal”) bettors, they will swoop in with large wagers on undervalued teams. Those won’t be profitable each time, but they will be profitable on average (if the odds are really skewed and the bookmaker doesn’t take too large a cut). Because these bettors can wager significant sums, they have incentives to corrupt the game (such as throwing boxing matches) and to acquire perfectly legal information that is not widely known. In grain markets, for instance, large speculators pay to acquire such information by hiring private weather forecasters. They make money off people who don’t know whether it rained too much or too little on Iowa cornfields last night.

Why the Limits on Political Betting also Limit the Public’s Information

If speculators could make large political bets, their incentives would be similar to sports bettors and commodity speculators—corrupt ones to throw contests and legitimate ones to acquire better information, such as conducting their own polls and focus groups. If they could make large bets and believed the presidential race would come down to Florida and Pennsylvania, they would concentrate on gathering data there. As they made bets on that information, their inside knowledge would be reflected in the public odds and so would inform the rest of us.

That doesn’t happen in political markets because there is no financial incentive for those bettors to collect additional information, if acquiring it costs time or money. They can’t make large enough bets to recoup their additional investment. That means the political odds you and I read do not incorporate as much information as it could. They are better than polls, even polling averages, but they could be better if the markets were deeper and accepted large wagers.

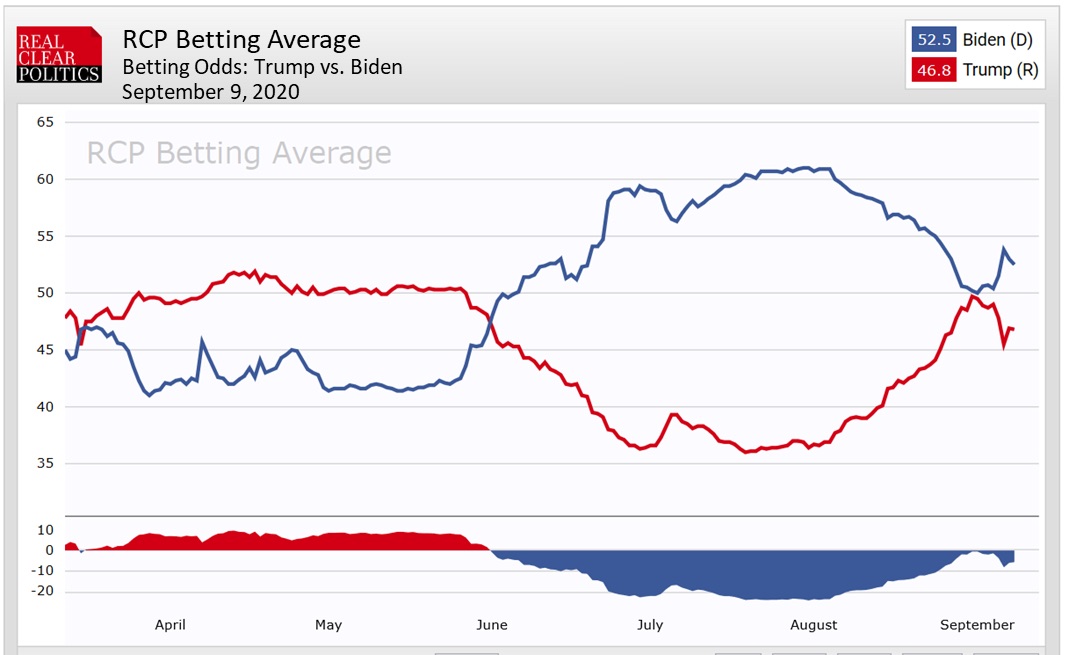

What Are the Odds Now? How Have They Changed?

The most comprehensive aggregation shows Biden leading by about 6 points on Sept. 9, with a 52.5% chance of winning. That number is culled from seven British oddsmakers and then averaged, just as Real Clear Politics does for opinion polls. Another site, which averages three sites, shows Biden with a 9-point lead. The two aggregators move in tandem, naturally, though their odds differ slightly because they rely on different betting sites.

The odds, like polls, are snapshots in time. The only way to see how a race is evolving is to look at several over time. Those changes have been dramatic since Biden effectively clinched the nomination in early March.

- In mid-March, the odds showed Biden and Trump tied. The presidential race began dead even.

- By late April, Trump had taken an 8-point lead, which he held for a month.

- In late May, Biden began closing rapidly. He took the lead in early June.

- Over the summer, the former vice president’s lead increased significantly.

- By late July, when Biden’s lead peaked, his odds of winning were more than 25 points higher than the incumbent’s. Bookmakers placed Biden’s chances of winning at over 60 percent, Trump’s at under 40%.

- Beginning in mid-August, Trump began a steady climb, erasing Biden’s lead.

- By Aug. 31, the two candidates were back in a virtual tie, just as they had been when the race started.

- That trendline changed dramatically over Labor Day weekend, when Trump was hit by anonymous allegations he disparaged servicemen and women. Amid the controversy, Biden not only reversed his decline, he rose to an 8 point lead.

- Over the past two days, the gap has closed to 6 points.

Bottom Line on the Betting Line

Betting markets are more accurate and timely than even the best polling averages. But the two are complements, not substitutes. Betting markets build on political polls, as well as other information.

Watching these markets closely has two advantages for political observers:

- They are timelier since the odds reflect the latest news, which may take days to show up in polls; and

- They are probably more accurate since the odds incorporate both polling data and other information.

Useful as political markets are, they could be better. That will happen only if U.S. laws change so people who know more can wager more. When they can, the odds will better reflect all available information, public and private, and everyone will have a clearer understanding of where the races really stand.

Charles Lipson is the Peter B. Ritzma Professor of Political Science Emeritus at the University of Chicago, where he founded the Program on International Politics, Economics, and Security. His recent articles for The Bridge include an analysis of recent statements by the presidential candidates and an examination of conformity on college campuses. He can be reached at charles.lipson@gmail.com.

Comments are closed.